dumb money (ep. 1): credit cards

reframing the value we derive from credit cards

Part II – Anime Monographia")

Hi friends! Welcome back to dumb money!

The driving principle behind this series is simplicity.

I believe that as long as we direct our efforts toward developing high-value habits, it’s possible to win the money game with minimal time and effort.

With that in mind, let's chat about credit cards.

Here are some questions we’ll explore:

How can you extract 90% of the value of having a credit card by doing just 10% of the work?

How should you go about choosing the best card for your needs?

Is it worth dedicating time and effort into churning credit card points?

What’s the credit card application process like?

What easy-to-implement habits will set you up for long term success?

As a heads up: I don’t plan on giving credit card recommendations.

There are plenty of YouTubers, websites, and Reddit posts that dive into that area of expertise. But to address the elephant in the room, here are the cards that I use:

Bilt Mastercard: for rent

Venture X: for travel

Apple Card: for everything else

These cards keep me engaged with my finances without making me feel like I need to carry my cards around in a Yu-Gi-Oh duel disk any time I go out for coffee.

Without further ado, let’s dive into the world of credit cards.

Money not lost is money gained.

This one might come as a shocker. 90% of the value you derive from a credit card comes from the money you save by:

1) Paying your card balance in full each month

2) Not missing any payments

Let me explain in more detail.

enjoying this piece so far? if you haven’t already, click the button below to make sure that you receive my next piece in your inbox. and if you want to read more of my posts, check them out here!

Paying your card in full saves you from incurring exorbitant interest charges.

Credit card interest rates are one of the highest you’ll encounter; they can range anywhere between 15-30% based on your credit-worthiness.

The graphic below illustrates that paying off a $1,000 credit card balance with minimum payments incurs $990 in interest charges.

That’s insane!

Essentially, you're nearly paying double the original amount owed, and that doesn't even account for the ongoing issue of your credit card balance increasing month by month due to new purchases.

I’m not going to elaborate any more on this topic of credit card interest and debt anymore. If you are facing these high interest charges, you need to pull it together and prioritize taking actionable steps to get yourself out of it ASAP.

If you’re fortunate enough to not have any credit card debt, let's keep it that way by following this simple mantra:

Always pay your full credit card balance.

Your credit score can make or lose you tens of thousands of dollars.

While recurring card interest charges may eat up your hard earned cash in the shorter term, missing payments breeds a different beast: a poor credit score.

Your credit score can make or lose you tens of thousands of dollars.

That’s because credit scores are directly tied to the interest rates you are offered when you take out a loan to buy a car, home, or any other big purchase. People with good credit scores get more affordable rates offered to them, which can save tens of thousands of dollars in the long run.

When you’re young and just starting out, chances are, your score won’t be very high. Here’s the good news: it's not hard to build it up.

There are a few things that factor into your credit score, but the easiest way to improve it is to build a long history of on-time credit card payments.

In other words, by simply starting to use a credit card as early as you (responsibly) can AND paying things off on time, you’ll put yourself in a great position to have a strong credit score in a few years.

In case you couldn’t tell, I want everyone reading this to be in the 760+ FICO score range by the time we reach our 30s. No matter how hard you work, you’ll probably never make $192k a day like Shohei Ohtani does. But a 760+ credit score? Totally achievable.

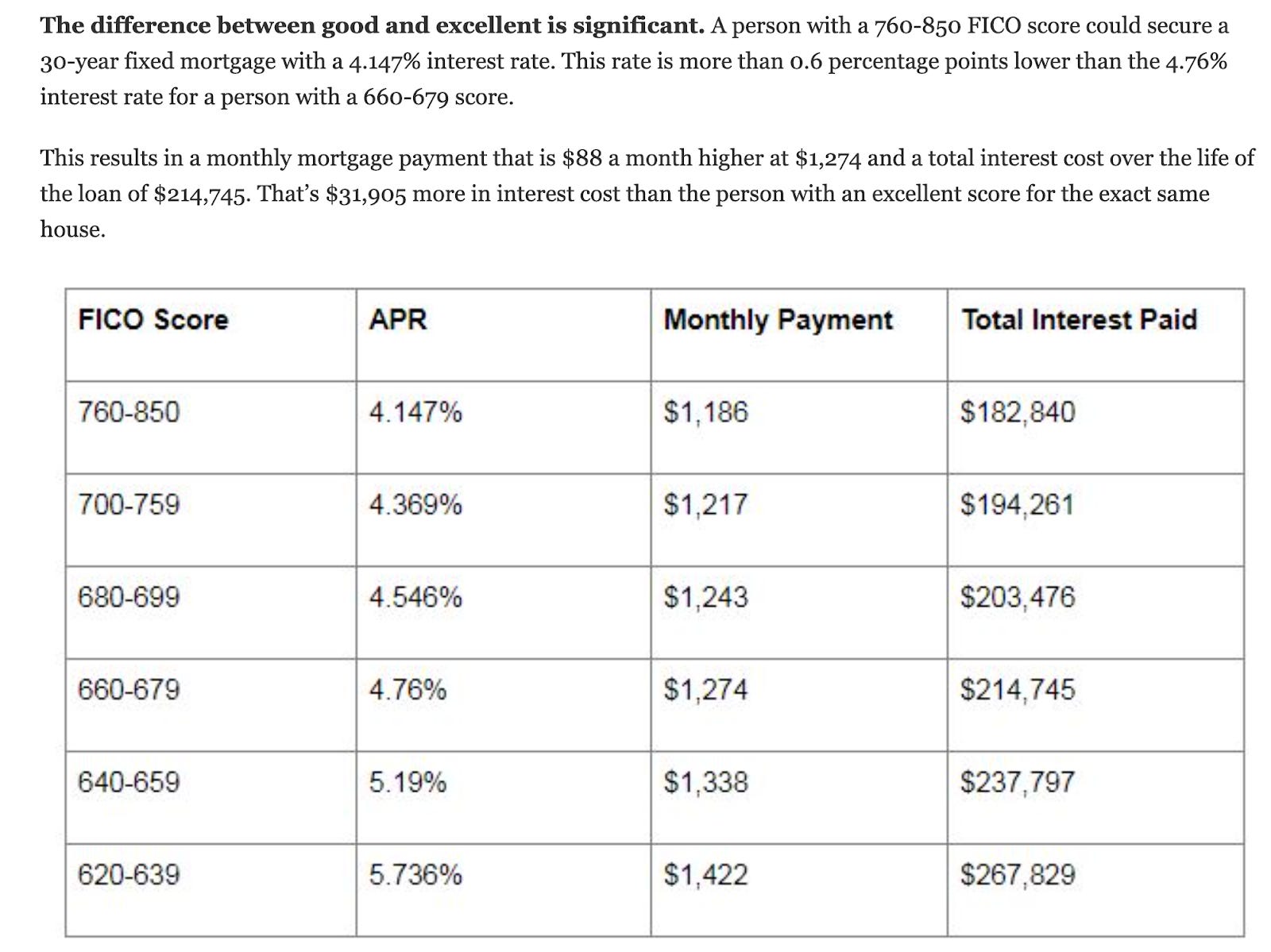

To give you a sense of the truly immense financial repercussions of bad credit, let’s take a look at some numbers. The table below shows average interest payments relative to your credit score range:

Let’s say Friend A and Friend B are in their mid-30s and purchase identical homes:

Friend A has a very good FICO Score of 760.

Friend B has the Millenial average score of 690.

Based on the table above, over 30 years, Friend A pays $21,000 less on their mortgage than Friend B.

It’s truly remarkable how much an interest rate difference of 0.4% makes when you’re working with a lot of money over a long period of time. Friend A, simply by maintaining a strong credit score, has $21,000 more in her bank account than Friend B.

This interest rate difference is not exclusive to homes. Friend A surely will receive better rates for when she purchases a car or takes out any loan in general, all because she prioritized good, credit-building habits.

Credit card points maximizing is overrated.

I know, credit cards are sexy because of the free money they promise.

But the truth is, the rewards are so marginal that no matter how many credit card points you earn, you won’t notice any lifestyle change.

I can speak from personal experience. My quality of life has not changed AT ALL since I started playing the credit card game. Sure, sometimes I get to sit in an airport lounge for half an hour before a flight, but that’s about it.

There are two reasons why credit card points-maxing is not really worth it:

Reason #1: You earn credit card points by buying things with your card and getting a percentage back for each purchase. Simple as that. But when you’re in your 20s, you’re probably not making that much money (loser) and thus not spending much (broke boy). The quantity of points and free flights you can earn is restricted by how much you can spend. Assuming a 2% cash back card, in order to earn just $20 in credit card benefits, you’ll have to spend $1,000.

Reason #2: Let's say you've conducted thorough research and meticulously optimized your credit card rotation strategy. You have a designated credit card for shopping, another for dining, one more for flights, and so on. All in all, you’ll make a couple hundred dollars more a year than someone who uses a simple cash back credit card. In other words, you’ll make about a buck a day for your efforts.

Here’s the truth.

People who own a bunch of credit cards operate on FOMO, but they also think of points-maxing as a hobby. It’s truly a weird psychological phenomenon.

But I get it. It’s human nature to gain satisfaction from getting a good deal, and in a world filled with expensive hobbies (golf) to pathetic ones (pickleball), credit card churning is a fine one to engage in. It’s not really up to us to judge people for doing something they enjoy, is it darling?

Once you’ve gotten into the groove of paying your cards in full and on time, it’s worth it to ask yourself, “Am I willing to put in the time and effort to participate in this credit card hobby?”

I play the credit card game. I do what I can to maximize points. But that’s only because I find it genuinely fun.

However, if the thought of strategizing over which credit card to use or figuring out how to best transfer points to airlines fills you with dread, then please, don't let it get to you. There's no need to stress over such trivial matters.

You’re not missing out on much.

A simple cash-back card will do the job.

Just like in dating, you’re not going to be eligible for every credit card in the market. But having a higher income and credit score will give you more options to choose from.

The easiest way to get a sense of whether a card is a good fit for you or not is to check if your credit score falls within the ideal credit score range for that card. You can check your credit score with your bank or on credible sites like experian.com.

Broadly speaking, there are two types of credit cards: cash-back cards and travel cards.

Cash-back cards are simple. If a card offers you a flat 2% cash-back, then you can effectively think that anything you spend on that card is 2% off. There are a lot of no annual fee options.

Travel cards are a bit more complicated. They often have annual fees, can give 5-10x points for travel-related purchases, and offer more benefits. In general, the rewards system can get pretty complicated. Oftentimes, the best way to redeem points gained through travel cards is through transferring points to partner airlines and booking big international flights through them.

If you’re just starting off, get a no annual fee card that offers 1.5-2% cash back on all purchases for everyday use.

Even with all the “fancy” cards I have, I use my 2% cash back card the most.

Once you get the hang of using your cash back card and find yourself flying at least a couple times a year, it might be a good idea to consider adding a travel card into the mix as well.

Additional Category 3: Student and Secured Cards

Some of you may apply for credit cards and get denied because you don’t have enough credit history. In that case, you may have to start with credit cards that are labeled as “Student Cards” or “Secured Cards”.

Think of these as beginner cards; they’ll probably give you less cash back and charge you higher interest rates. You should know by now that neither of these two things matter much as long as you’re paying off your card fully and on time.

If these are the only types of cards you qualify for, then go for it. They’re great tools for demonstrating your credit worthiness. Stick through these for a year or two, then apply for that traditional cash-back card.

enjoying this piece so far? if you haven’t already, click the button below to make sure that you receive my next piece in your inbox. and if you want to read more of my posts, check them out here!

Is applying for a credit card annoying?

Annoying is subjective, but the credit card application process takes a few minutes tops. The only thing you might not know off the top of your head is your income and SSN.

Two words of advice on opening and closing credit cards:

Don’t close your old cards. If you already have a credit card and decide to open a new one, don’t close your old account. Length of credit history factors into your credit score, so closing your old accounts will harm your credit score.

Apply through pre-approval, rather than through direct application. Check if you’re pre-approved for a card before you apply for it. Applying for too many cards and getting rejected by them will harm your credit score.

Once you decide on a card that works for you, look up that card’s name followed by “pre-approval”. You will be taken through a very similar application flow to what you would go through if you were to apply directly for that same card. After you finish the application, you’ll be provided a list of cards you’re eligible for.

If the card you wanted isn’t listed there, it means you would’ve been rejected had you applied directly. That’s fine, let’s find another one that might work for your needs.

If you do see the card you wanted, great! There should be a button somewhere that allows you to complete an abbreviated application.

Automatic payments are the biggest credit card hack and will solve all your problems.

Pretty much every credit card supports autopay. This means linking your card to a bank account and setting it up such that whenever your statement is due, your balance is auto paid in full.

This is the solution, the answer, the key to the two most important “accidents” people make with their cards.

If you enable this option, you will NEVER forget to pay on time, and you will NEVER not pay the full balance you owe (when setting autopay up, make sure you select the “pay statement balance” option, not the “pay minimum balance” one).

Your bank account and your credit score will thank you.

Here are the key points we went over today:

A credit card is worth getting because it will allow you to build your credit and get better rates when you make larger purchases like a car or home

You can get 90% of the benefit of a credit card by choosing a simple cash-back card and paying it off in full and on time

Points maxing is a valid way to earn free money, but you’ll need to enjoy it as a hobby because you can’t make much money off of it

The best way to make sure you’re staying on top of your payments is to set up automatic payments

Here are some action items:

Do a bit of research and open a simple cash-back credit card (1 hour)

Check your credit score to get a sense of where you are now (15 minutes)

Set up automatic recurring credit card payments (10 minutes)

Remember, the best investment in our 20s is in ourselves. Building new skills, traveling to places you haven’t been, focusing on your career, meeting new people; these should be our priority. Let’s create a simple credit card system that works and move on with our lives.

Thanks for tuning into this week’s dumb money episode!